Bitcoin ETFs see heavy outflows as Binance OTC volume surges

Public wrappers leak capital while private desks absorb large trades, price discovery shifts away from order books

Images

Bitcoin ETFs Cap Week With $225 Million Outflow as Ether Hits 8-Day Slide

news.bitcoin.com

Bitcoin ETFs Cap Week With $225 Million Outflow as Ether Hits 8-Day Slide

news.bitcoin.com

Bitcoin ETFs Cap Week With $225 Million Outflow as Ether Hits 8-Day Slide

news.bitcoin.com

Bitcoin ETFs Cap Week With $225 Million Outflow as Ether Hits 8-Day Slide

news.bitcoin.com

Bitcoin ETFs See $171 Million Outflow as Ether Extends Losing Streak

news.bitcoin.com

Bitcoin ETFs See $171 Million Outflow as Ether Extends Losing Streak

news.bitcoin.com

Bitcoin ETFs See $171 Million Outflow as Ether Extends Losing Streak

news.bitcoin.com

Bitcoin ETFs See $171 Million Outflow as Ether Extends Losing Streak

news.bitcoin.com

Binance OTC Spike Reveals Intensifying Institutional Grip on Crypto Liquidity

news.bitcoin.com

Binance OTC Spike Reveals Intensifying Institutional Grip on Crypto Liquidity

news.bitcoin.com

Binance CEO: Digital Assets Are Becoming a Core Part of Modern Finance

news.bitcoin.com

Binance CEO: Digital Assets Are Becoming a Core Part of Modern Finance

news.bitcoin.com

Binance CEO: Digital Assets Are Becoming a Core Part of Modern Finance

news.bitcoin.com

Binance CEO: Digital Assets Are Becoming a Core Part of Modern Finance

news.bitcoin.com

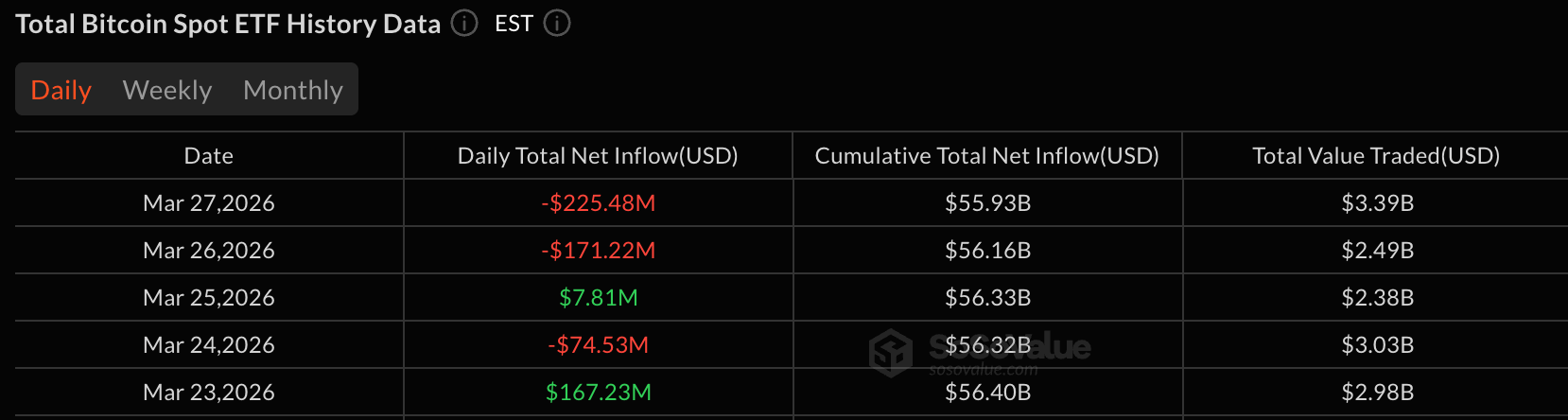

Bitcoin spot ETFs ended the week with roughly $225 million in net outflows on Friday, while Binance says its OTC desk has already reached about a quarter of last year’s volume in the first two months of 2026. According to Bitcoin.com, BlackRock’s IBIT accounted for most of the ETF selling, while ether ETFs extended an eight-day streak of withdrawals.

The two datapoints point in opposite directions for the same market. Public vehicles meant to make crypto easier to buy—US-listed spot ETFs—are seeing redemptions that show up as clean daily flow numbers. At the same time, Binance is advertising a surge in off-exchange execution, where large trades are negotiated privately and settled without printing through the visible order books. Binance CEO Richard Teng said on X that institutional demand for “deep liquidity and trusted execution” is rising, and the exchange’s OTC report highlights a $105 million conversion from WBETH to ETH completed in two hours.

That split matters because it changes what “price discovery” looks like. ETF flows are transparent but blunt: they aggregate many decisions into a single number and often force a mechanical response in the underlying market. OTC flow is the opposite: it can be large, fast, and largely invisible until after settlement, and it is designed to minimise slippage and avoid signalling. When more trading migrates into private channels, the screen price becomes less informative about where size can actually be done, and retail participants are left watching a thinner public order book.

It also changes who carries which risks. OTC desks promise discretion and execution quality to large counterparties, but they concentrate operational and counterparty exposure in a handful of venues and banking relationships. The same report frames bitcoin’s $60,000 level as a focus for institutional positioning and argues the “floor is likely not far below,” language that reads less like a market quote and more like a sales pitch for clients deciding where to place size.

Meanwhile, the ETF tape shows the other side of the trade: the willingness of allocators to pull money from the regulated wrapper when performance or risk appetite turns. Bitcoin.com reports no offsetting inflows on Friday, despite billions of dollars in trading volume, and net assets falling with the withdrawals.

In a market that advertises transparency as its upgrade over legacy finance, the fastest-growing execution channel is the one that produces the least public information. On Friday the visible product saw hundreds of millions leave, and the least visible venue said it was busier than ever.