Hormuz disruption threatens fertiliser supply

Urea shipments and LNG feedstock depend on the strait, Food inflation arrives after planting decisions are locked in

Images

Fishers work in front of oil tankers in the Strait of Hormuz in 2018 (AP)

independent.co.uk

Fishers work in front of oil tankers in the Strait of Hormuz in 2018 (AP)

independent.co.uk

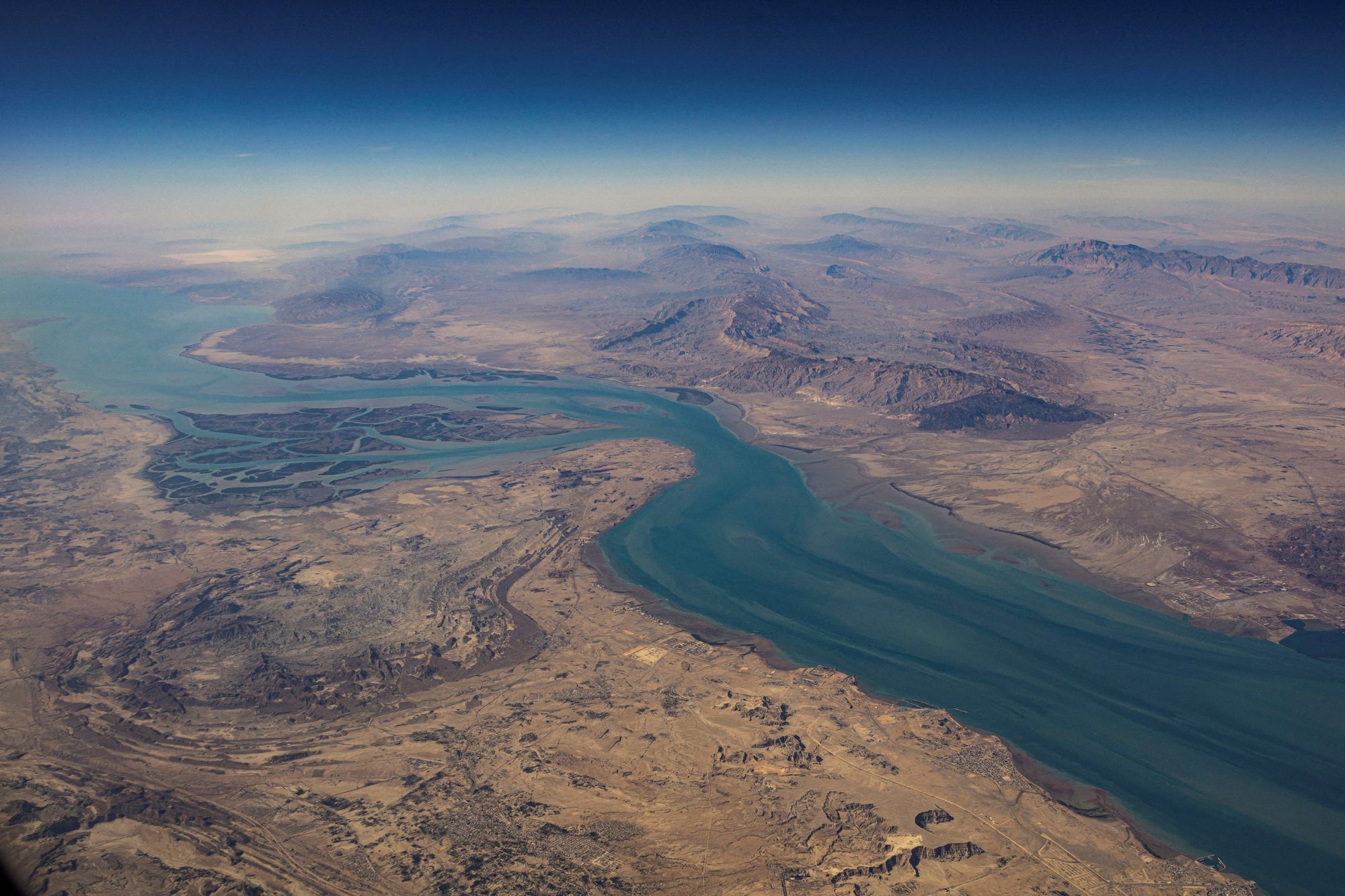

The Iranian shores and the island of Qeshm in the Strait of Hormuz (Reuters)

Reuters

The Iranian shores and the island of Qeshm in the Strait of Hormuz (Reuters)

Reuters

Roughly a third of globally traded urea passes through the Strait of Hormuz, according to an analysis republished by The Independent from The Conversation. As the Middle East war drives insurers to pull war-risk cover and pushes shipping firms to reroute or wait, the immediate market focus has been oil. The fertiliser channel is slower-moving, but it is built on the same chokepoint.

Nitrogen fertiliser is manufactured from natural gas. The Haber–Bosch process turns methane into ammonia, and ammonia into products such as urea that underpin modern crop yields. The Persian Gulf sits at the centre of that system for two reasons the authors highlight: cheap gas and decades of capital investment in export-oriented ammonia and urea capacity in countries such as Qatar, Saudi Arabia and the UAE. When Hormuz becomes difficult to insure and finance, it is not only crude and LNG cargoes that stall; it is also the inputs for the next planting season.

The timing matters. In the northern hemisphere, fertiliser purchases accelerate ahead of planting. A delay of weeks can be disruptive; a disruption of months forces farmers into choices that show up later as lower yields. The Independent piece notes that even modest reductions in nitrogen application can produce disproportionately large declines in output, potentially translating into millions of tonnes of lost crops. That does not hit supermarket shelves tomorrow; it hits after harvest, when inventories are already committed.

The dependency is wider than it looks on paper. India runs domestic urea plants but relies heavily on LNG imports from the Gulf to power them. Brazil depends on imported nitrogen and phosphate fertilisers to sustain soybean and maize production. Even the United States, despite being a major fertiliser producer, imports meaningful volumes. In practice, “self-sufficiency” often means domestic factories tied to imported gas, imported feedstock, or imported shipping capacity.

The first-order shock is logistical and financial: freight rates rise, war-risk premia widen, and cargoes become harder to insure. The second-order shock is agronomic: reduced fertiliser use lowers yields. The third-order shock is political: once food inflation arrives, governments tend to reach for price caps, subsidies, and emergency procurement—tools that shift costs onto taxpayers and further distort supply.

Oil prices can fall as quickly as they rise when shipping normalises. A missed fertiliser window cannot be replayed.