Middle East airspace closures disrupt global travel

Oil and shipping insurers reprice risk as Hormuz fears return, Tax-funded naval protection quietly caps the premium

Images

Iranian and Israeli airspace has been closed (Flightradar)

Flightradar

Iranian and Israeli airspace has been closed (Flightradar)

Flightradar

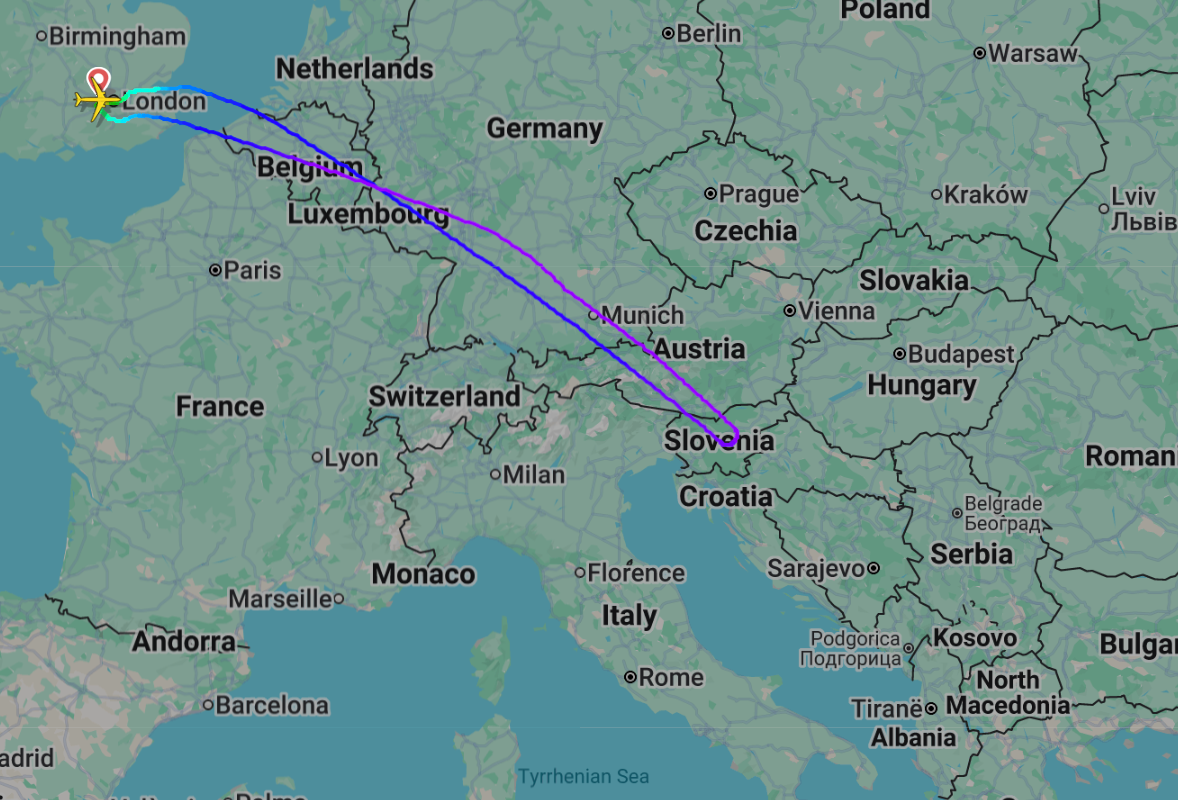

A British Airways flight to Doha returned to London (Flightradar)

Flightradar

A British Airways flight to Doha returned to London (Flightradar)

Flightradar

The US and Israel have carried out a series of strikes on Iran (AP) (AP)

independent.co.uk

The US and Israel have carried out a series of strikes on Iran (AP) (AP)

independent.co.uk

Air routes over Iran and Iraq were abruptly shut this weekend after US and Israeli strikes on Iran, forcing airlines to cancel flights, turn aircraft around mid‑journey and reroute traffic over Saudi Arabia. Dubai International Airport—normally handling roughly a quarter of a million passengers a day—suspended flights, while Qatar Airways halted operations to and from Doha, according to The Independent.

The immediate disruption is visible on flight‑tracking maps, but the larger economic story is the speed at which geopolitics becomes a line item. When airspace closes, aircraft burn more fuel on longer routings, crews and planes miss rotations, and airlines pay for extra handling, accommodation and compensation. The same mechanism applies at sea: shipping insurers raise war‑risk premiums, vessels pay more for fuel and detours, and schedules slip through ports and distribution networks. Those costs do not stay with the carrier; they are passed through as higher freight rates and higher prices for time‑sensitive goods.

Oil is the clearest transmission channel. Sweden’s Svenska Dagbladet reports crude prices rising on fears the conflict could disrupt flows through the Strait of Hormuz—the narrow passage out of the Persian Gulf through which about a quarter of the world’s seaborne oil trade passes, along with much of Qatar’s LNG exports. Even without a blockade, the market prices the possibility: tankers demand higher charter rates for risky routes, insurers charge more to cover hull and cargo, and refiners pay a premium to secure supply. For economies already sensitive to energy costs, that risk premium shows up quickly in transport, food and industrial inputs.

Governments then enter the pricing chain. Naval patrols, air-defence deployments and crisis logistics reduce the probability of disruption, but they also shift part of the cost from shippers and insurers onto taxpayers. Commercial actors can buy insurance; they cannot buy a carrier strike group. The result is a two‑tier market in which private firms pay higher premiums while states provide the backstop that keeps the system functioning—and, in doing so, mute the full price signal that would otherwise force faster rerouting of trade, inventory rebuilding, or demand destruction.

For households and central banks, the practical question is not whether a wider war happens, but how long the risk surcharge persists. A week of diversions is an operational headache; a month of elevated war‑risk pricing becomes inflation, and inflation becomes wage pressure, rate expectations and slower growth.

In the hours after airspace closures, flights to Dubai, Doha, Amman and Bahrain were cancelled or turned back. The Strait of Hormuz remained open, and the oil market moved anyway.